by Michael Blanding

Starting companies is becoming so quick and cheap that venture capitalists have shifted strategy funding entrepreneurs. Now, more startups get backing—but they have to prove themselves in a hurry, according to research by Ramana Nanda and colleagues.

As cloud technologies allow startups to build companies faster and cheaper than ever before, venture capitalists are rethinking who and how many companies they finance, according to recent research.

Enter the era of “spray and pray,” where venture firms over the last decade have seeded more firms than previously, but with less upfront investment of time and money. As someone who teaches entrepreneurial finance, Harvard Business School Professor Ramana Nanda wanted to find out if this new strategy has paid off for investors and their portfolio companies.

Nanda and colleagues present their findings in a paper scheduled to appear in a forthcoming issue of the Journal of Financial Economics, titled Cost of Experimentation and the Evolution of Venture Capital, co-written with Michael Ewens of the California Institute of Technology and Matthew Rhodes-Kropf of MIT Sloan School of Management.

The researchers focus on one of the most important technological shifts in recent years—the introduction of Amazon Web Services, which has allowed startups to cheaply rent server space and development tools in the cloud and scale up as needed rather than purchasing their own expensive hardware and software.

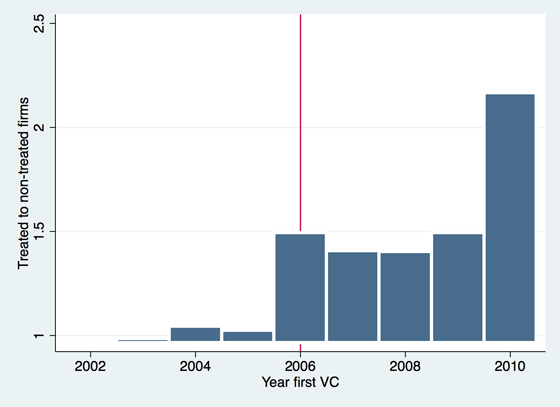

By comparing rates of investment before and after AWS was introduced in 2006, Nanda and his colleagues could see how VCs changed their strategies with startups such as cloud-based software and service companies, which could take advantage of AWS to decrease costs, versus others like biotechs that were less impacted by the new technologies.

After the 2006 introduction of Amazon Web Services, VC first-round investment in firms helped by the technology (“treated” firms) grew to twice the number of investments per year than in other, or “untreated” firms. (Source: “Cost of Experimentation and the Evolution of Venture Capital”)

“The goal was to try and understand whether VCs were allocating their capital to a larger number of startups with a smaller amount of money to each,” says Nanda. “Equally important, we wanted to see if they were just investing in a lot of worse firms, or if these long-shot firms were actually higher in value if they succeeded.”

The researchers found that the number of startups receiving first-round funding increased substantially between 2006, when AWS was introduced, and 2010, especially for those firms that could most take advantage of cloud services. For the control group of companies in industries such as aerospace and medical devices, first-round funding increased from 350 to 450 firms, a rise of 30 percent. But for startups in the software and media industries that could make use of AWS, funding increased from 375 to 700 firms, a nearly 100 percent rise.

Of the firms that Nanda and his colleagues looked at over the period of 2002 to 2010, 43 percent failed before receiving a second round of funding. They found that failure rates increased after the introduction of cloud computing in 2006, implying that although money was being spread to more firms, many of them were failing before they received a second round of funding—a phenomenon that became known as the “Series A Crunch.”

“The benefit is that [today] more firms are being funded,” says Nanda. “In the past, you would be less likely to fund a long-shot bet because it would not be profitable. Now, because it’s so cheap to start companies, you can be willing to give more firms a try, and shut them down quickly if they don’t work out.”

On the positive side, the firms that did succeed substantially increased their valuation after second-round funding, implying that the spray and pray approach has been effective in identifying long-shot companies that show real promise over and above what was expected.

As one example, Nanda cites Airbnb. “You might think it was not going to work to put money into a firm that rents out mattress space on the floor. But then it turns out it actually does, and Airbnb becomes a super-valuable company,” he says. “Airbnb would have been very hard to be backed in the previous period because it was such as long-shot bet.”

The strategy does have some drawbacks, however. Among them is the concern that with the rapid-fire approach to funding, VCs have been less likely to fill their traditional role of providing advice and guidance to startups, putting less resources into firm governance.

For instance, the researchers found that for the group of firms they looked at, VCs were 14 to 21 percent less likely to place an investor on the board of directors in the first round of financing/funding.

“It shifts the governance to the later stages of the company,” says Nanda, “in part because it’s not really worth it for VCs to dedicate a lot of time and resources into that when the rate of failure is so high.” Some of that slack, he adds, has been picked up by accelerators such as Y Combinator or Techstars, which are able to provide guidance to startups as a group, offering them business and technical advice until they are able to prove themselves and grow to a size that a VC is willing to invest more time and money into ensuring their success.

Another worry with the spray and pray approach is that by emphasizing investments in companies that can prove their worth quickly, VCs may be underfunding other more complex types of startups that require more time to bear fruit.

“One of the challenges with this approach is it really directs attention of investors to projects where you can learn cheaply and quickly,” says Nanda, “so it may disproportionately de-emphasize those problems that are more complex and where it is more costly to learn.”

It’s unclear whether those types of startups are being underfunded on an absolute basis or merely a relative basis compared with faster projects—that is, says Nanda, if the number of companies in more complex industries such as clean technology stays the same while the number of software companies increases, then the approach is still a net benefit. If, however, the number of complex companies that get funded decreases in favor of quicker and easier companies, then that could signal a problem. Nanda hopes to address this question in future research.

On the bright side, he says, technological innovations have come so quickly in recent years that there are few industry sectors that have not seen their development costs dramatically decrease. For example, CRISPR technology has allowed gene editing in biotech, 3D printing has allowed for rapid prototyping for hardware startups, and reusable rockets have brought down the cost to build and launch a small satellite to under a million dollars.

“And we often see advances in one area power technological advances in another,” says Nanda. “Supercomputing has opened up massive innovations in nuclear startups by allowing us to simulate the inside of a nuclear reactor for a mere $200 million instead of $6 billion!” As new technologies such as artificial intelligence, machine learning, and virtual reality bring more advances, the cost to fund startups will only get lower, and the number of startups that can get a shot to succeed can only increase.

“With the pace at which each of these innovations are influencing other innovations,” says Nanda, “it’s a fascinating time to be an entrepreneur or an investor.”

工业4.0创新平台 版权所有 All Rights Reserved, Copyright© 2013- 京ICP备14017844号-3

评论